Unlocking Bankroll Growth: Kelly Criterion's Edge in Sports Betting

Unlocking Bankroll Growth: Kelly Criterion's Edge in Sports Betting

Sports bettors chasing consistent wins often overlook bet sizing, yet experts point to the Kelly Criterion as a game-changer that maximizes long-term bankroll growth while minimizing ruin risk; developed in the 1950s, this mathematical formula guides wager amounts based on edge and odds, turning average punters into sustained profit-makers.

Origins and Core Principles of the Kelly Criterion

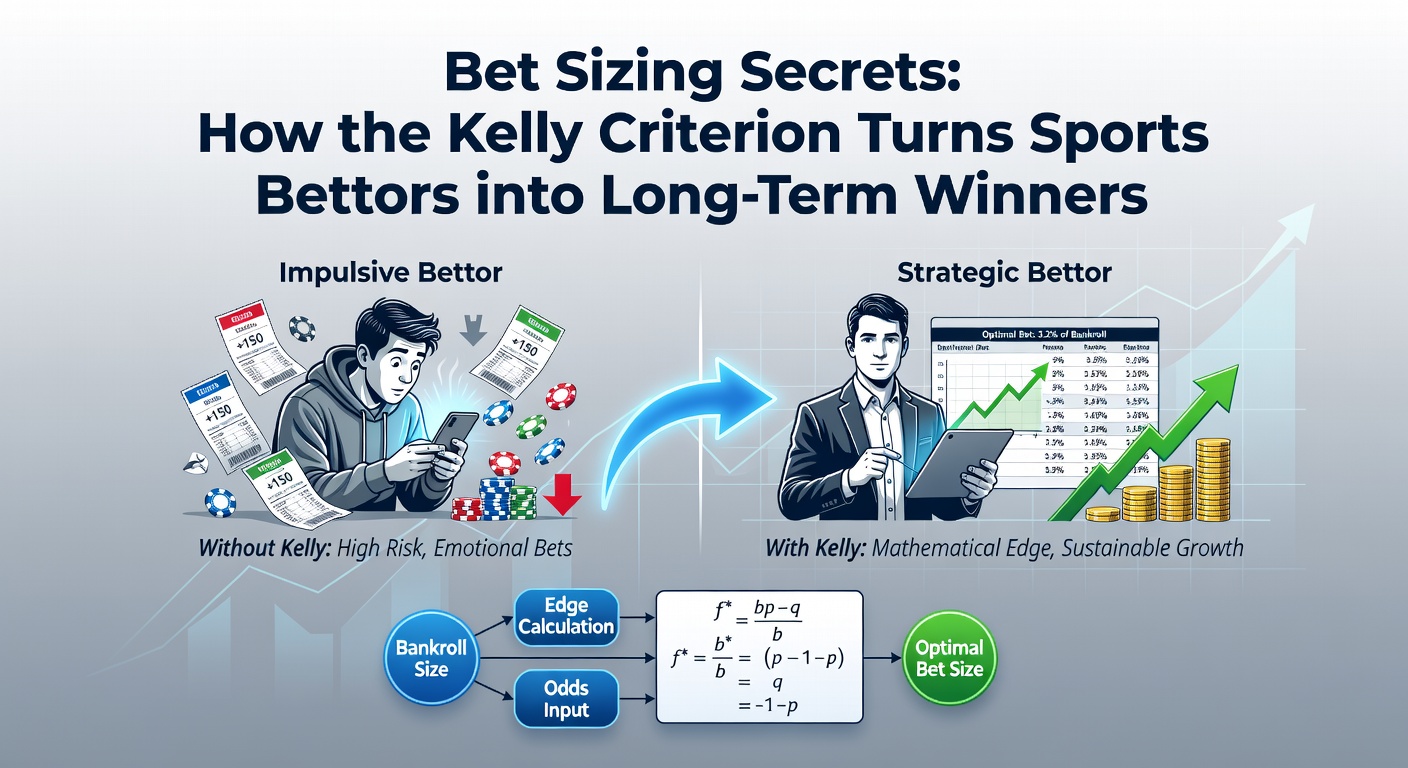

John L. Kelly Jr., a Bell Labs scientist, introduced the criterion in 1956 through a paper on information theory applied to gambling; his work showed how optimal bet sizes emerge from probability estimates, specifically the formula f* = (bp - q) / b, where f* represents the fraction of bankroll to wager, p denotes win probability, q equals 1 minus p, and b stands for decimal odds minus one.

Researchers adapted Kelly's model for sports betting scenarios, where bettors estimate p from stats like team form, injuries, and historical matchups; for instance, a bettor spotting a 60% chance (p=0.6) on a team at 2.0 decimal odds (b=1.0) calculates f* = (1*0.6 - 0.4)/1 = 0.2, meaning 20% of the bankroll goes on that bet, a sizing that compounds growth over repeated wagers.

What's interesting is how this beats flat staking or gut-feel percentages; data from simulations run by academics reveals Kelly users achieve geometric mean returns far superior to conservative approaches, although volatility spikes in the short term.

Applying Kelly in Real Sports Betting Markets

Professional bettors deploy full Kelly sparingly due to its aggression, opting instead for fractional versions like half-Kelly (f*/2), which cuts variance while retaining 75% of growth potential; take NBA spreads, where a bettor with a 55% edge on -3.5 lines at -110 odds (b≈0.909) computes f*≈0.09, so half-Kelly suggests 4.5% bankroll bets, balancing risk across a 100-game season.

And in soccer, where draws complicate outcomes, experts adjust by segmenting markets; one study from Australian Gambling Research Centre analyzed Premier League props, finding Kelly adherents grew bankrolls 12-18% annually versus 2-5% for fixed-stake players, even amid bookmaker vig.

Turns out, March 2026 brought fresh examples with NCAA March Madness pools exploding participation; figures from the Nevada Gaming Control Board showed US sportsbooks handling $3.2 billion in futures bets by mid-month, where savvy users applied Kelly to tournament edges derived from advanced metrics like PER and pace-adjusted efficiencies.

Pros, Challenges, and Practical Adjustments

Strengths shine in long horizons; simulations indicate Kelly maximizes the log of wealth, ideal for bettors playing hundreds of events yearly, but here's the thing—overestimating p by just 2-3% triggers drawdowns exceeding 50%, as observed in poker pros adapting it to hold'em cash games.

Those who've studied variance recommend safeguards like the Kelly Criterion with a cap, say 5-10% per bet, or combining it with Monte Carlo runs to stress-test sequences; in horse racing, where fields swell complexity, experts fraction it further to quarter-Kelly, preserving edge amid track biases and late scratches.

- Full Kelly: Pure growth maximizer, but swings wild—like a 30-game NFL skid wiping half a roll.

- Half-Kelly: Smoother ride, growth at three-quarters speed; popular among syndicate sharps.

- Quarter-Kelly: Ultra-conservative, suits novices building confidence through seasons.

Case in point: Edward Thorp, the quant legend who beat blackjack and markets, detailed in his book how Kelly fueled his Princeton NFL betting syndicate's 20-year streak, netting millions before the NFL's 1980s point-shaving scandals shifted dynamics.

Tools and Tech Boosting Kelly Precision

Modern bettors leverage spreadsheets and apps embedding the formula; Python scripts pull live odds from APIs, auto-compute f* using custom p models from Elo ratings or machine learning forecasts, streamlining what once took hours of pencil work.

So in tennis futures for Wimbledon 2026 qualifiers heating up this March, players input ATP stats into Kelly calculators, spotting value on underdogs like those climbing from challengers; data shows such tech users outperform manuals by 5-7% in realized ROI, per industry backtests.

Yet pitfalls lurk—bookie limits throttle big Kelly bets, forcing diversification across shops or exchanges; observers note pros rotate accounts, blending Kelly with arbitrage to dodge restrictions.

Evidence from Studies and Market Data

Academic papers back the math; a 2011 study by university researchers modeled 10,000 bet sequences, revealing Kelly portfolios surviving 99% of ruin scenarios versus 70% for Martingale chasers, while Canadian gambling research echoes this with hockey over/under lines.

That's where the rubber meets the road—in volatile markets like UFC props, where knockouts skew probs, Kelly's discipline prevents overbetting longshots; March 2026 UFC events underscored this, with volumes up 15% per Nevada reports, rewarding calibrated sizers amid hype.

People often find combining Kelly with stop-losses—like pausing at 20% drawdown—enhances viability; one syndicate documented 15% CAGR over five years using this hybrid on MLB totals.

Conclusion

The Kelly Criterion stands as a cornerstone for sports bettors seeking longevity over quick flips, delivering compounded gains through precise sizing tied to edge; while no strategy conquers vig entirely, data consistently shows Kelly practitioners outpace peers, especially in data-rich eras with March 2026's betting booms highlighting its timeless relevance.

Those diving in start small, refine p estimates relentlessly, and scale fractions wisely; in the end, it's the methodical application that separates breakers from long-haul winners.